Written By: Brian Deal

At DVIRC, we recently conducted a poll during our Supply Chain 101 program involving over 120 supply chain professionals to gather insights on current inventory management practices and challenges. The findings from our SC101 sessions reveal significant trends and areas for improvement in inventory management. Here’s what we discovered and how your business can benefit from these insights.

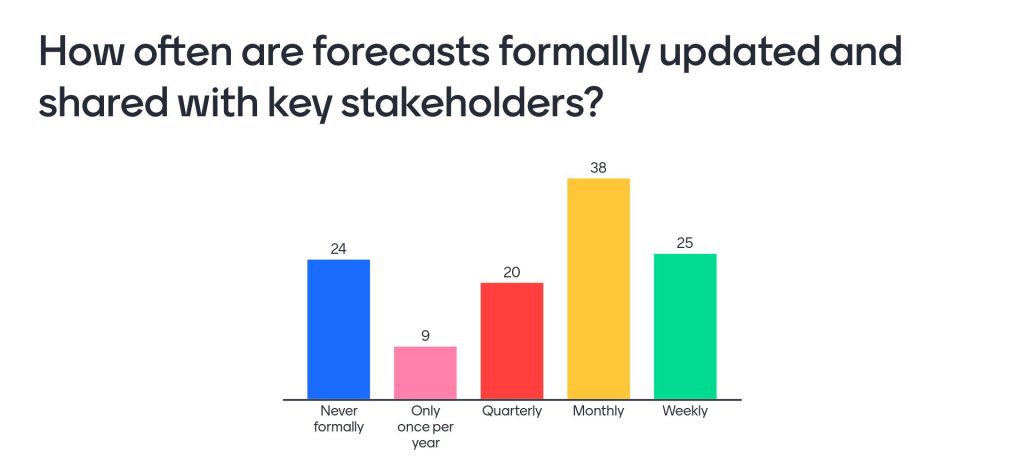

Are You Flying Blind with Your Inventory?

According to our survey, 28% of respondents either never conduct a formal forecasting process or do so only once a year. This lack of regular forecasting can leave businesses flying blind, leading to stock outs, obsolescence, and poor customer service levels. Without a structured approach to forecasting, companies are at risk of making uninformed decisions that can disrupt supply chains and customer satisfaction.

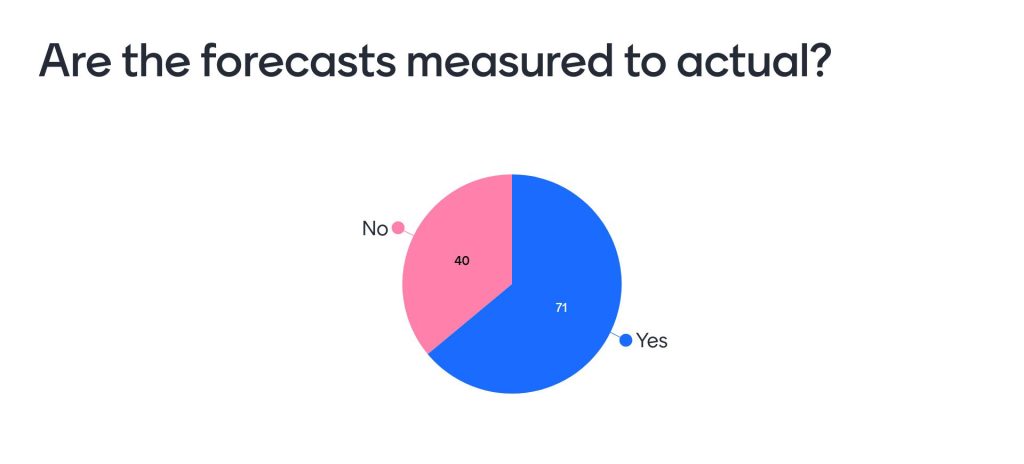

Measuring Forecasts: A Necessity, Not an Option

Another critical insight is that over one-third of businesses are not measuring their sales and operations forecast against actual outcomes. This high degree of variation between planned and actual performance can result in higher costs and inefficient supply chains. Measuring and understanding this variation is essential. Without it, companies cannot identify inefficiencies or areas for improvement, leading to unnecessary expenses and potential service failures.

A significant number of businesses lack an understanding of their inventory variation. However, reducing variation can offer substantial economic advantages. The acceptable level of variation varies by industry – for instance, Fortune100 companies may aim for a 2-3% variation while typical consumer packaged goods may tolerate around 10%.

Business owners should ask themselves: Do you know what’s acceptable for your industry? What value could be unlocked by reducing your variation?

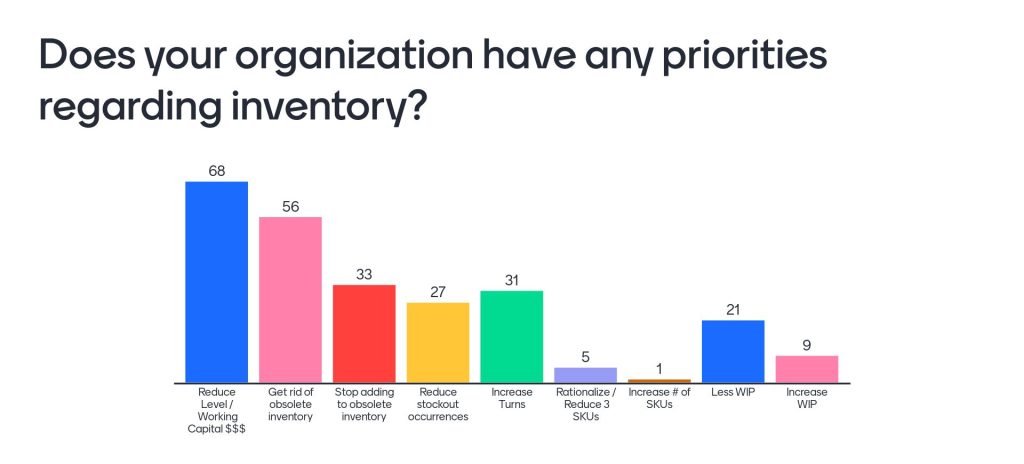

The Economic Value of a Robust Inventory Strategy

Over half of the respondents recognized the economic value that a well-defined inventory strategy can bring to their organization. As interest rates rise and carrying costs increase, businesses face additional pressure to manage inventory effectively. Implementing strategic inventory programs can help mitigate these costs and add significant value to the organization.

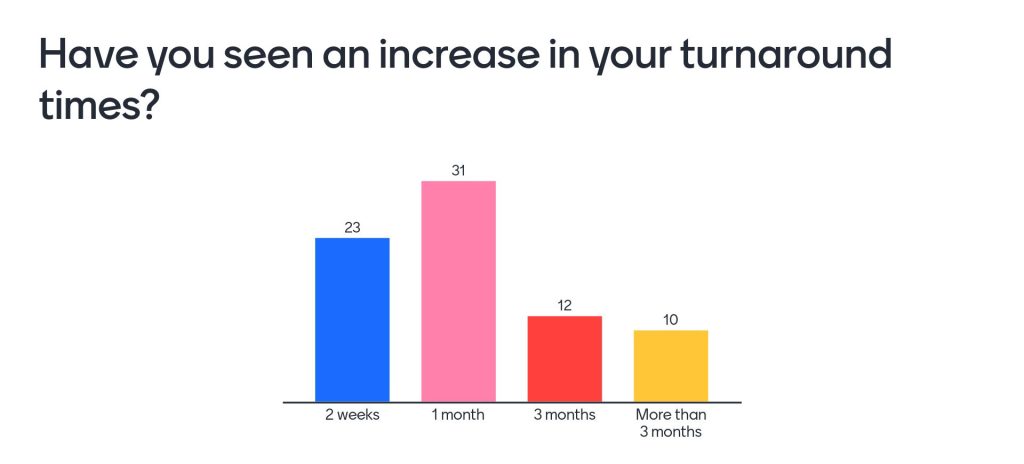

Rising Lead Times: A Growing Concern

The survey also highlighted a concerning trend: lead times and overall turnaround times are increasing. This escalation puts additional strain on cash flow and service levels, making it more challenging for organizations to maintain efficient operations. Addressing these delays requires proactive measures, including supplier relationship management and process optimization.

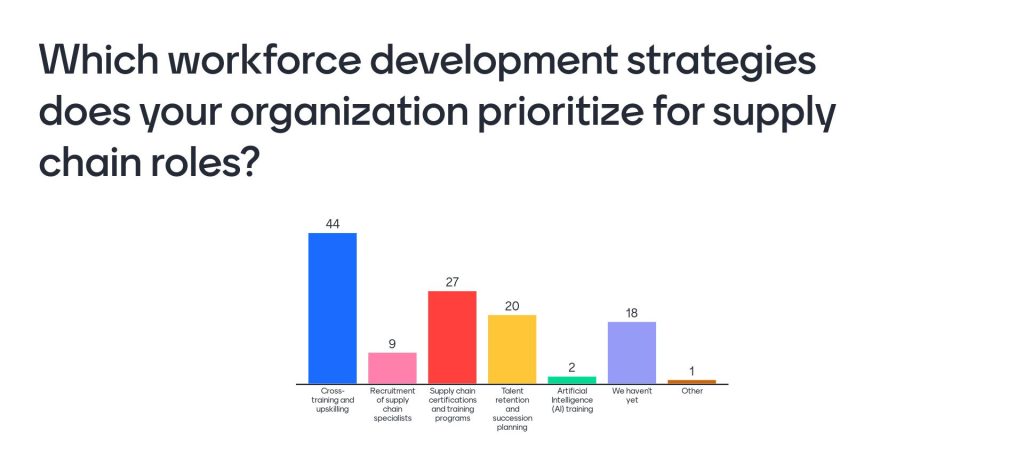

Investing in People: The Key to Success

Lastly, businesses are recognizing the importance of investing in their workforce. Cross-training and certification programs are becoming increasingly popular as companies strive to upskill their employees from novice to advanced levels. This investment in human capital not only improves operational efficiency but also fosters a culture of continuous improvement and innovation.

The insights from these results underscore the importance of regular forecasting, performance measurement, and strategic inventory management. By understanding and addressing variation, implementing robust inventory strategies, and investing in their workforce, businesses can navigate the complexities of inventory management and drive economic value. As interest rates and lead times continue to rise, these strategies will be essential for maintaining competitive advantage and ensuring long-term success.

This article is written by Brian Deal, DVIRC’s Director of Strategy and Supply Chain Services. For more information or to schedule a complimentary supply chain assessment with Brian, please contact us.