This is a guest article from PNC

The exclusion amounts currently available for the federal gift and estate tax and generation-skipping transfer tax, sometimes individually or collectively referred to as transfer tax(es),1 may prove to be a once-in-a-lifetime opportunity to pass significant wealth to children, grandchildren, and more distant generations in a tax-efficient manner. Individuals and families wishing to capitalize on this tax-saving opportunity may have to act fast since the currently expanded exclusion amount is set to expire at the end of 2025. Moreover, the exclusion amount may change even earlier if Congress enacts legislation reducing the exclusion amount before then.

As discussed below, we recommend that individuals and families for whom intra-family gifting is part of their wealth planning strategy:

- consider making meaningful transfers of wealth now, before the exclusion amount changes;

- confirm that other planning objectives are met before undertaking further gifting; and

- where appropriate, incorporate flexibility into wealth transfer plans to address possible changes in legislation or changes to personal and financial circumstances.

We suggest that you discuss these recommendations with your legal and tax advisors.

The Current Opportunity

The Tax Cuts and Jobs Act of 2017 (TCJA)2 created a significant opportunity to tax-efficiently transfer wealth to the next generation and beyond, effectively doubling the gift and estate tax exclusion and the generation-skipping transfer tax exclusion from the limits in effect in 2017. The exclusion amount is indexed for inflation and for 2023 is $12.92 million per person ($25.84 million for a married couple) and is subject to further adjustment for inflation through 2025. For individuals and families willing and able to make significant gifts, this represents an unprecedented opportunity to transfer assets to younger generations at a much-reduced transfer tax cost.

This increased gifting capacity is not permanent. Assuming no changes, the current exclusion amount (as further adjusted for inflation) is set to expire on December 31, 2025. Beginning January 1, 2026, the exclusion amount will be decreased to $5 million, indexed for inflation. Although the exclusion amount in 2026 had been projected to be approximately $6.4 million, increased inflation may render that estimate obsolete. If today’s elevated inflation rates continue for the next three years, it is possible that the exclusion amount in 2026 could be approximately $8 million per person.3

To Gift or Not to Gift?

For individuals and families who wish to pass assets to children, grandchildren, and (perhaps) more distant descendants as part of their overall wealth transfer plan, gifting now, rather than later, could provide significant benefits to the family. Yet lifetime gifting is a balancing act, where the benefits of making gifts today should outweigh the potential disadvantages. Determining whether to make substantial gifts to future generations is a complex decision and is dependent on a number of factors.

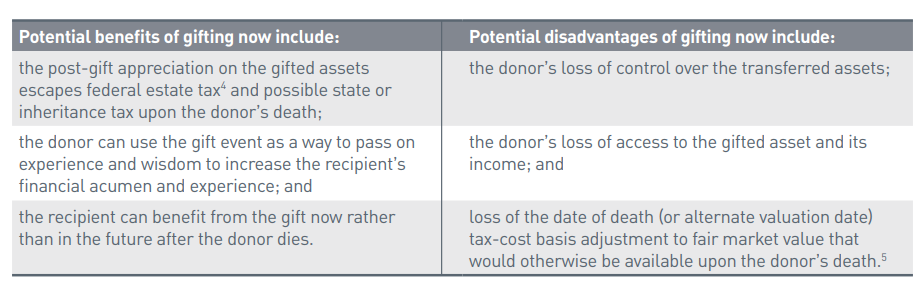

For many, thoughtful planning can capture many of the advantages of lifetime gifting while minimizing the impact of potential disadvantages, such as the few pros and cons of gifting that are highlighted in the graphic above. A discussion with your tax, legal, and financial advisors can help you decide what is right for you and your family.

Considerations in Light of Impending

Exclusion Reduction Assuming the benefits of gifting now outweigh the potential drawbacks, and an individual or family is in a position to make significant gifts, the taxpayer should keep the following in mind when determining how much (and how) to gift before this window of opportunity closes.

Go Big, or Don’t Bother

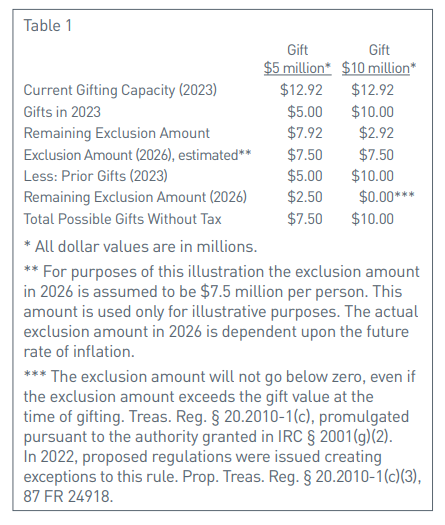

Having decided to take advantage of the expanded exclusion amount, determine whether the value of the gifts is substantial enough to make best use of this unique opportunity. Because prior use of the exclusion amount reduces a taxpayer’s exclusion amount available to offset future gifts, gifting less than the anticipated reduced exclusion amount does not maximize the current gifting opportunity (Table 1).

It is important to note that if the exclusion amount is reduced in the future, making gifts now will not increase the donor’s future taxable estate. This is because the Internal Revenue Service issued regulations in 2019 (known as the “anti-clawback” regulations) that eliminate the risk of an increased taxable estate solely from a decrease in the exclusion amount.6

Keep All Planning Goals in Mind

While gifting now can create transfer tax savings for a taxpayer’s family, take care that these benefits don’t come at the expense of meeting other financial goals, both now and in the future. For example, making large gifts to family members now may impair the donor’s ability to maintain a desired lifestyle or contribute to charity. Likewise, confirm that recipient children and future generations are prepared to handle financial assets before making large gifts. Using trusts to make significant gifts can help prevent recipients from getting too much, too fast. Trusts can also be designed to provide asset protection that may not be available for outright gifts. Additionally, trusts can serve as a teaching tool to help prepare current and future beneficiaries to successfully manage wealth.

Maintain Flexibility

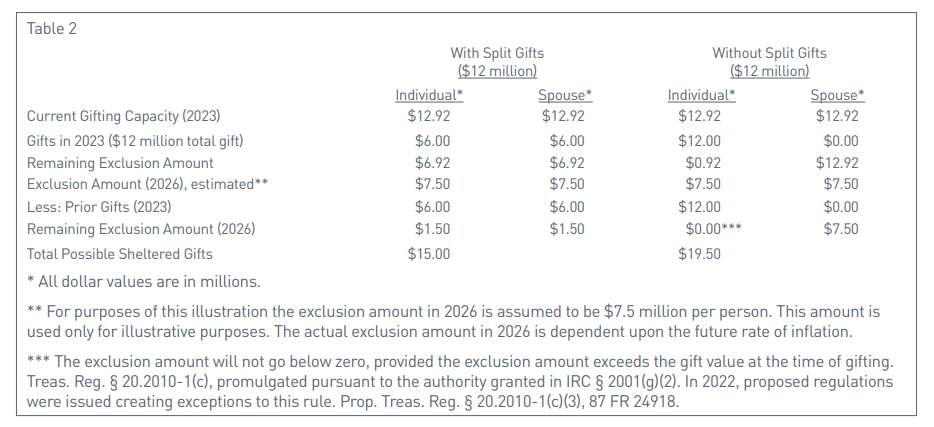

Because the rules can change at any time, maintaining flexibility with regard to gifting is important. Married couples who wish to preserve as much future gifting capacity as possible may want to consider not electing to split gifts7 and to use the gifting capacity of just one spouse. While this would preclude the donor from making additional gifts in excess of the donor’s remaining exclusion amount (if any) without actually paying a gift tax, the total gifting capacity for the couple would be increased because the exclusion amount for the nondonor spouse is preserved for future use (Table 2).

Another option that may provide flexibility is the use of trusts that can benefit the donor’s spouse (as opposed to a trust that only benefits the donor’s lineal descendants), sometimes referred to as a spousal lifetime access trust.8 This giving strategy may provide some access to the gifted funds to the spouse (and through the spouse, the donor and the family) should the need arise. Unfortunately, this strategy and the one discussed above are only available to married couples. There are few strategies that provide significant flexibility for unmarried individuals when making large current gifts.9

What to Gift

In addition to deciding how much to gift and when, determining the optimal assets to gift can increase the tax benefit to the family. Transferring the following

types of assets may provide some further advantages when it comes to gifting.

Assets Expected to Appreciate in the Near Term

One of the benefits of gifting during one’s lifetime is the ability to remove future appreciation from the

taxpayer’s taxable estate at death. Gifting assets that are expected to appreciate in the near term may provide an advantage over assets that are expected to

appreciate more slowly.

Assets Subject to Valuation Discounts

Gifting assets that are subject to valuation discounts for lack of marketability or lack of control can help magnify the total value that can be transferred without additional transfer tax. For example, if an asset that would otherwise be valued at $10 million is subject to a valuation discount of 20%, this asset would be valued at $8 million for gift tax purposes. To put it another way, transferring assets subject to a 20% valuation discount can allow a taxpayer to transfer assets worth $12.5 million at a gift tax value of $10 million.10

Family Business Interests

The specter of gift taxes can be a significant deterrent to transferring a business to the next generation. Likewise, selling the business to the next generation may require earmarking future business cash flows to pay the sales price, potentially hampering the ability to preserve and grow the business. If a family transition is desired and the business is to continue, it may make sense to consider gifting some or all of the ownership interests in the family business. This transfer may also be eligible for valuation discounts. This can help to leverage the value of assets transferred to the next generation while preserving capital within the business.

Act Before the Window of Opportunity Closes

Gifting requires careful consideration and is not something to undertake lightly, but the benefits of lifetime gifting can be great. If lifetime gifting fits into your wealth transfer plan, consider taking advantage of the current expanded gift and estate tax and generation-skipping transfer tax exclusion amounts before they expire or are otherwise reduced. Contact your financial, legal, and tax advisors to see which gifting strategies can best help you reach your financial goals.

Endnotes

1 For a discussion of gift and estate taxes and the generation-skipping transfer tax, see Subtitle A, Part VI: Increase in Estate and Gift Tax Exemption, Joint Committee on Taxation, General Explanation of Public Law 115-97, December 20, 2018, https://www.jct.gov/publications.

html?func=startdown&id=5152 (last accessed October 31, 2022).

2 Pub. L. 115-97.

3 After expiration of these provisions of the TCJA, the gift and estate tax and the generation-skipping transfer tax exclusion amounts revert to $5 million per person, indexed for inflation beginning from 2010. Internal Revenue Code (IRC) § 2010(c)(3)(B)(ii). The 2026 exclusion amount used herein is an estimate, based on future inflation assumptions.

4 Only growth in the value of the transferred asset(s) occurring after the gift escapes transfer tax, since the value as of the date of the gift will be added back to a decedent’s future taxable estate, pursuant to IRC §2001(b)(1)(B).

5 26 USC § 1014. See also “Income Tax Basis in Property Received,” in Subtitle A, Part VI: Increase in Estate and Gift Tax Exemption, Joint Committee on Taxation, “General Explanation of Public Law 115-97,” December 20, 2018, https://www.jct.gov/publications. html?func=startdown&id=5152 (last accessed October 31, 2022).

6 Treas. Reg. §20.2010-1(c), promulgated pursuant to the authority granted in IRC § 2001(g)(2). On April 27, 2022, The U.S. Department of the Treasury issued proposed regulations containing exceptions to this rule. The rule would not apply to certain transfers included in the donor’s gross estate, transfers made by enforceable promise, and other amounts that are duplicated in the tax base. Also excepted would be items that would have been included in the donor’s gross estate but for the transfer, relinquishment or elimination of a power or interest within 18 months of death. Prop. Treas. Reg. § 20.2010-1(c)(3), 87 FR 24918 (April 27, 2022).

7 See, IRC § 2513.

8 At its most basic description, the SLAT strategy is a gift from one spouse (the donor spouse) to an irrevocable trust for the benefit of the other spouse (the beneficiary spouse) and, perhaps, others. The beneficiary spouse can receive distributions from the SLAT, yet the SLAT is designed to be excluded from the beneficiary spouse’s gross estate and to not be subject to estate tax when the beneficiary spouse dies. The donor spouse can also allocate the exemption amount from the generation-skipping transfer tax to the SLAT, making the value of the gifted assets and any subsequent appreciation in their value exempt from future estate tax for many generations. Of course, each family and each family’s plan is different. Trusts can be complicated, and should not be entered into without obtaining advice. Creating any type of trust involves legal, tax and financial considerations. You should consult your legal, tax and other advisors to determine if creating a SLAT is right for your family and how creating a SLAT would impact your goals and plans.

9 Taxpayers who are not married may have a more difficult time transferring assets while retaining some indirect access to them. Those taxpayers could consider creating self-settled, asset protection trusts in states that allow for their creation, such as Delaware or Ohio. E.g., 12 Del. C. §§ 3570, et seq.; Ohio Rev. Code §§ 5816.01, et seq. Such trusts allow the creator of the trust to be a discretionary beneficiary of the trust while not subjecting trust assets to the claims of the beneficiary’s creditors or causing the value of the trust to be included in the creator’s gross estate and subject to estate tax when the creator dies. These trusts are not without controversy and care should be taken when creating and maintaining them. Additionally, other states may not respect the purported creditor protection aspects of the trust. See, generally, In re Huber, 493 B.R. 798 (Bankr. W.D. Wash. 2013), further proceedings, Waldron v. Huber (In re Huber), 2013 Bankr. LEXIS 4981 (Bankr. W.D. Wash. 2013), aff’d, 2014 U.S. Dist. LEXIS 94574 (W.D. Wash. 2014).

10 The amount of valuation discounts, if any, should be determined by an appraisal performed by a qualified appraiser. Cf., Treas. Reg. § 301.6501(c)-1(f).